Two inches of water on the floor looks the same whether it came from a burst pipe upstairs or a flooded street outside.

Your insurer sees two completely different claims.

One gets paid. The other gets denied – sometimes for reasons buried in policy wording you've never read.

Here’s how the classification works, what each scenario costs, and what to do in the first 24 hours.

Key Notes

Insurers classify damage by source and path – internal water gets paid, external floods get denied.

Standard homeowners policies exclude flood, surface water, groundwater, and most sewer backups by default.

Flood damage routinely costs 5–10x more than internal water damage due to contamination and scope.

The first 24 hours of documentation and mitigation determine your final claim payout.

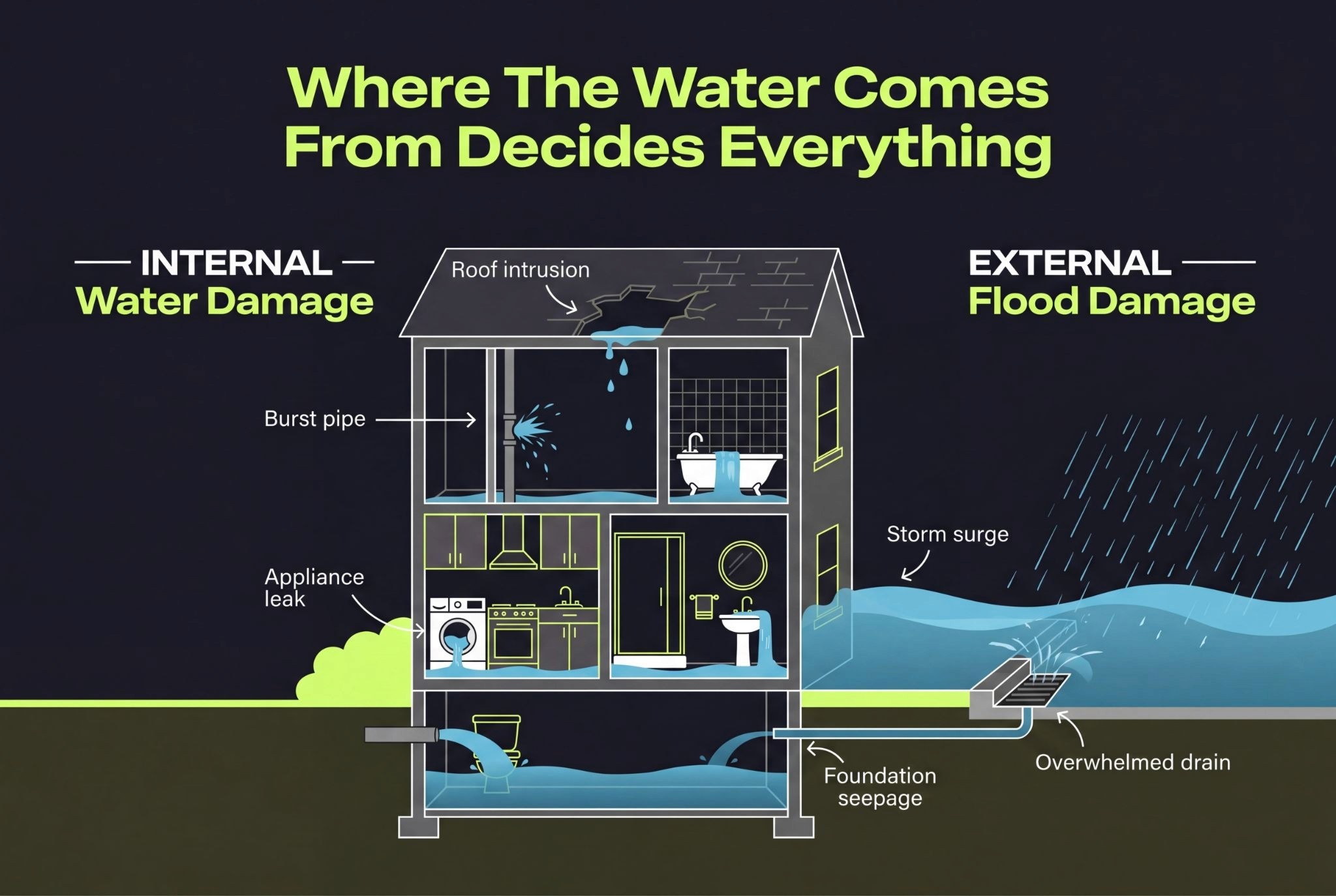

How Insurers Classify Water Damage vs Flood Damage

Insurers classify water damage vs flood damage based on source and path (not how much water is on the floor).

Here's The Practical Split:

Water Damage | Flood Damage | |

Origin | Inside the structure or from a specific covered event | External natural source – water rises over normally dry land before entering |

Scope | Usually confined to one unit, room, or section | Area-wide; multiple properties or large land area affected |

Typical examples | Burst pipe, ruptured water heater, wind-damaged roof leak, appliance failure | Heavy rain overwhelming drainage, river overflow, storm surge, surface water inundation |

Coverage | Generally covered by standard homeowners insurance | Excluded from homeowners; needs separate flood insurance |

The NFIP Definition Of "Flood" Is Specific:

Water (or mudflow) covering two or more acres of normally dry land, or affecting two or more properties.

The Simplest Test:

Did the water start inside or outside?

If it came from your plumbing, your roof, or an appliance – an adjuster will most likely call it water damage.

If it came across the ground from outside – it's flood.

What Causes Water Damage vs Flood Damage

The causes split cleanly along the same internal-vs-external line, and knowing them upfront helps you spot a misclassified claim before it costs you.

For NYC Property Managers, Both Are A Regular Part Of The Year…

The difference matters because a burst riser on the 14th floor and basement flooding from a Nor'easter feel like the same emergency at 2 AM, but they trigger entirely different insurance pathways.

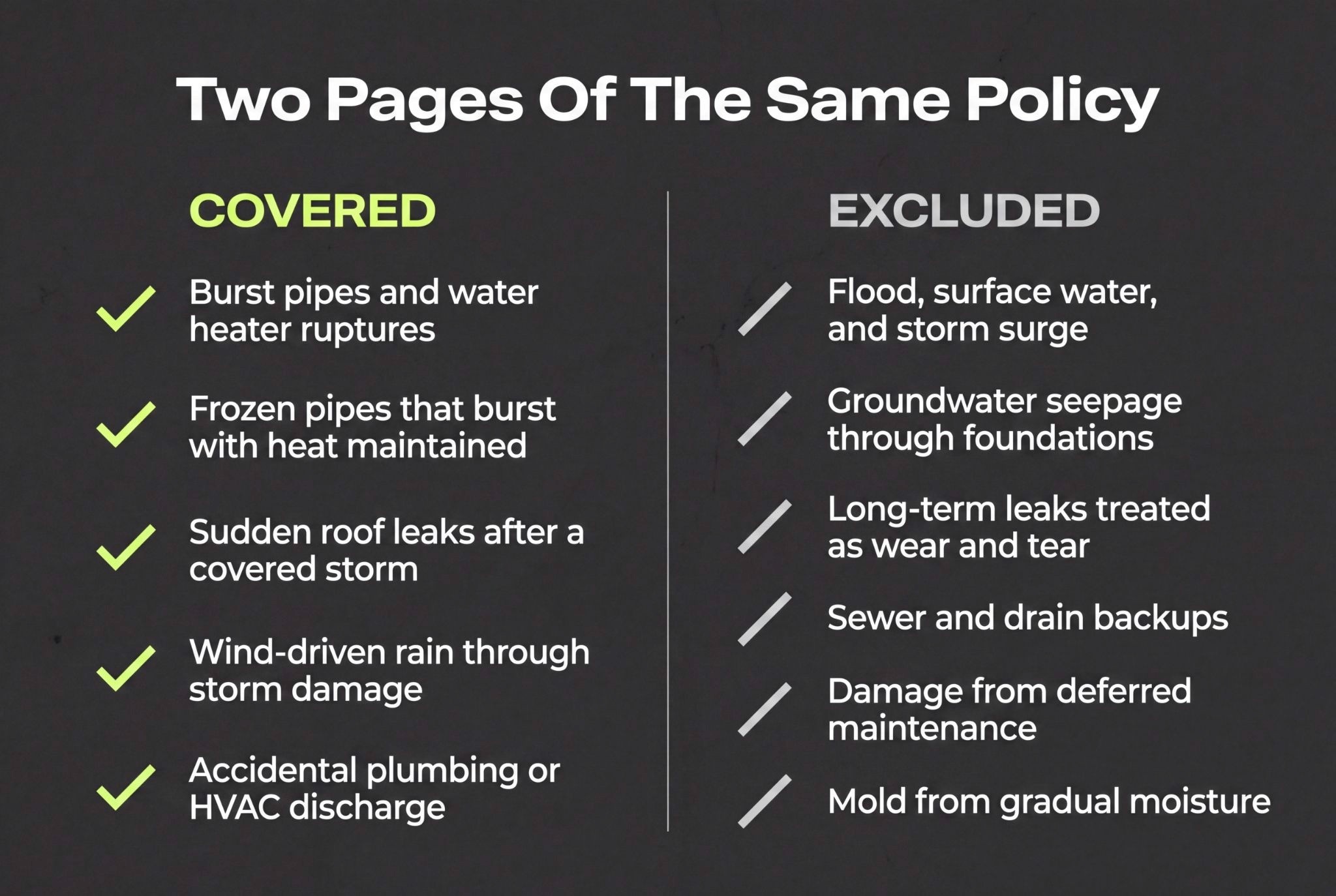

Insurance Coverage: What's Paid For & What Isn't

Standard homeowners insurance covers sudden, accidental water damage. It excludes flood almost universally.

Flood requires its own policy (usually written through FEMA's National Flood Insurance Program (NFIP) or a private flood insurer).

Why Flood Damage Is Excluded From Homeowners Insurance…

Flood gets carved out of standard homeowners policies by design. Insurers learned the hard way that flood doesn't behave like other perils – and pricing it into a standard policy would either crush premiums or sink the carriers themselves.

What The "Water Exclusion" Clause Excludes:

Standard homeowners policies contain specific water exclusion wording that carves out:

Flood and surface water

Tides and storm surge

Overflow of rivers, lakes, and other bodies of water

Groundwater and seepage

Sewer and drain backups (unless added back via rider)

Unless one of these is endorsed back into the policy, it's not covered (regardless of how the water got into your building).

How Flood Insurance Works

Flood insurance is a separate policy with its own rules:

Standard NFIP limits: $250,000 building / $100,000 contents (private flood policies often offer higher).

Waiting period: Typically 30 days before coverage kicks in – you can't buy it the day a hurricane is forecast.

Coverage: Structure, foundation, electrical, plumbing, HVAC, built-in appliances, and contents up to specified limits.

Rated on: Flood zone, elevation, and flood maps rather than standard underwriting.

Cost Differences: Water Damage vs Flood Damage

Water damage repairs typically run in the low thousands. Flood damage routinely pushes into five-figure rebuilds.

The same square foot of damaged drywall costs more when the water sitting in it was contaminated and stayed there for two days.

Typical Cost Ranges:

Damage Type | Typical Range |

Minor water damage (small leak, caught early) | $500–$2,000 |

Major water damage (multi-room, possible structural impact) | $5,000–$20,000 |

Flood restoration (multi-room, contaminated water) | $20,000–$40,000+ |

Severe whole-building flood | $50,000–$100,000+ |

These are order-of-magnitude figures and vary by region, contractor rates, and building type – but the gap between water damage vs flood damage cost is consistent across markets.

Why Does Flood Damage Cost More?

Three factors push flood costs up sharply:

Larger footprint. Floods affect entire rooms and floors, not just one ceiling section. More flooring, drywall, insulation, and contents have to come out.

Contamination. Floodwater is almost always Category 3 black water, carrying sewage, chemicals, and debris. That means demolition rather than drying. Porous materials get discarded, not saved.

Longer exposure. Floodwater sits for hours or days before it can be safely pumped out, wicking high up walls and saturating subfloors and structural cavities.

A clean burst pipe caught in two hours might cost $50–$70 per square meter to dry. The same area soaked in floodwater for 48 hours can run over $125–$200 per square meter, because materials have to be removed and replaced rather than dried in place.

Hidden Costs Property Owners Miss

Mold remediation surfacing weeks later ($800–$3,800 for typical jobs).

Wet insulation driving 15–30% higher heating and cooling costs until it's replaced.

Temporary tenant relocation in multi-unit buildings.

Contents sub-limits that leave gaps for electronics and high-value items.

Higher energy bills from compromised insulation that no one notices for months.

Water Damage vs Flood Damage: What To Do When It Happens

The first 24 hours decide both your claim outcome and your final repair bill.

The protocols for water damage vs flood damage overlap, but flood adds extra layers around safety, documentation, and paperwork deadlines.

For Water Damage…

Stop the source. Shut off the main water valve. Kill power if water is near outlets or the panel.

Document before cleanup. Wide-angle photos of every affected room, close-ups of the source, timestamped video with a brief spoken narrative.

Mitigate further damage. Extract standing water, move undamaged contents, set up fans and dehumidifiers if it's safe. Insurers expect "reasonable steps" – failing to mitigate can reduce your payout.

Notify your insurer within 24–48 hours with policy number, date of discovery, suspected cause, and rooms affected.

Get a licensed restoration contractor in immediately. Their moisture readings and reports become evidence.

For Flood Damage…

Don't enter until authorities clear it. Floodwater hides structural damage, contamination, and live electrical hazards.

Call your flood insurer before major teardown. NFIP guidance is firm on this – start the claim before stripping anything out.

Document high-water marks on walls, exterior silt and mud lines, and every damaged room and item before disposal.

Build a room-by-room contents inventory with approximate values.

Watch the Proof of Loss deadline – typically 60 days for NFIP-style policies. Miss it and your claim can be denied outright.

Water Damage vs Flood Damage FAQs

How long do you have to file a water damage claim?

Most insurers require water damage claims to be filed within 24–48 hours of discovery, though policies vary. Flood claims under NFIP have stricter rules – typically a 60-day Proof of Loss deadline. Check your specific policy wording, because waiting too long is one of the most common reasons claims get reduced or denied.

Does flood insurance cover basement flooding?

Flood insurance usually covers basement flooding when the water meets the NFIP definition of a flood (rising water from outside that affects two or more acres or two or more properties). Standard NFIP policies cover building elements like the foundation, electrical, and plumbing in the basement, but personal contents and finished walls often have limited or no coverage.

Can mold from water damage be covered by insurance?

Mold from water damage can be covered if it's a direct result of a sudden, covered event – like a burst pipe – and you took reasonable steps to dry out the property quickly. Mold from long-term leaks, gradual moisture, or deferred maintenance is almost always excluded. Many policies also cap mold coverage at a low sub-limit, often $5,000 or less.

How fast can a water damage restoration company arrive in NYC?

A licensed water damage restoration company in NYC should be on-site within 1–4 hours of a call for emergencies. Speed matters because mold can start developing in 24–48 hours, and insurers expect documented mitigation efforts. South Bronx Restoration runs 24/7 across the five boroughs with crews trained for both water damage and flood damage response.

Need Eyes On Your Property?

Licensed crews, IICRC-aligned drying & the documentation your insurer needs.

Conclusion

The water damage vs flood damage split comes down to one question every adjuster asks: where did the water start?

Inside the building from a pipe, appliance, or sudden roof breach – your homeowners policy usually pays. From outside the building, rising across the ground – that's flood and you're on your own without a separate NFIP or private flood policy.

The cost gap between the two is enormous, the documentation rules are different, and the 24-hour window after discovery shapes everything that comes next: payout size, repair scope, and whether mold turns a manageable loss into a six-figure rebuild.

If there's water in your NYC building right now, the smartest move is getting licensed eyes on it before mold sets in or your claim window narrows. We respond 24/7 across the five boroughs with the documentation your insurer expects. Get your free quote now.